USPAP Appraisal Review Compliance: What AMCs and Lenders Get Wrong and How to Fix It

Meta Description: USPAP appraisal review standards are widely misunderstood, and those gaps create real compliance exposure. Here’s what the rules actually require and where most operations fall short.

Compliance in the appraisal world is a topic that generates a lot of nods and not nearly enough action. Every AMC and mortgage lender will tell you they take USPAP seriously. Few can tell you exactly what Standards 3 and 4 require of their review appraisers or whether their current process actually meets those requirements.

This gap matters. Appraisal review compliance isn’t just an internal quality concern. It’s a line item on GSE audits, a factor in lender approval decisions, and increasingly, a focal point for regulatory scrutiny around appraisal bias and fair lending.

Here’s what the rules actually say, where most operations fall short, and what a compliant appraisal review process actually looks like.

The USPAP Framework for Appraisal Review

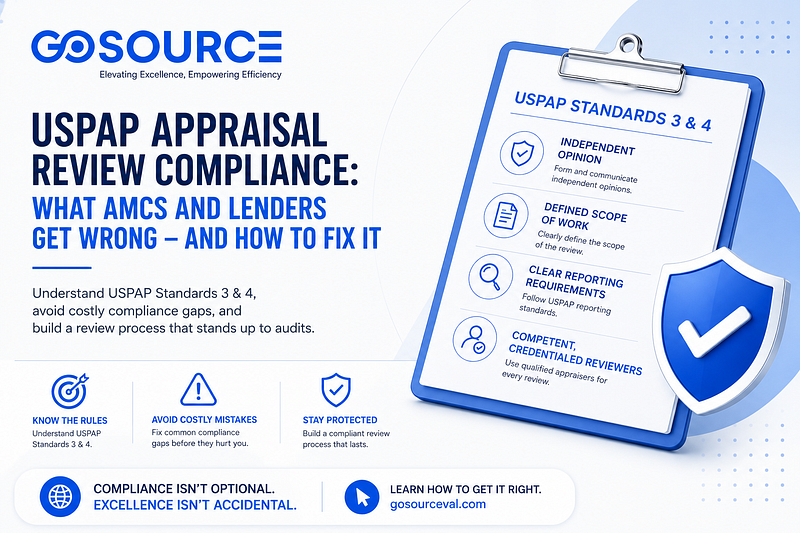

USPAP dedicates two full standards to appraisal review: Standard 3 (the development of an appraisal review) and Standard 4 (the reporting of an appraisal review). These standards establish what a review appraiser must do, what they must consider, and how they must communicate their findings.

The core obligation is straightforward: a review appraiser must form an independent opinion about the quality and credibility of the work under review, not simply verify that it follows a checklist.

Standard 3 requires reviewers to:

- Clearly identify the scope of work for the review assignment

- Not misrepresent the extent of their review

- Provide their own value opinion if the review assignment calls for one, and if they do, develop it as a separate, independent appraisal

Standard 4 governs the written review report, requiring reviewers to clearly communicate their opinions, the basis for those opinions, and any significant appraisal assistance received.

What the S disagrees with is every element of the original report. The reviewer’s job is to evaluate whether the work is credible and USPAP-compliant, not to redo the appraisal from scratch.

What AMCs and Lenders Most Commonly Get Wrong

After years in appraisal management, a few compliance gaps come up repeatedly. Understanding them is the first step toward fixing them.

Conflating QC Checklists with USPAP-Compliant Reviews

A QC checklist is a tool. It’s useful, efficient, and absolutely worth having. But running a report through a checklist is not, by itself, an appraisal review under USPAP. A compliant review requires the reviewer to form and communicate independent professional opinions, not just mark boxes as complete or incomplete.

When AMCs label their checklist outputs as “appraisal reviews” in their documentation and client communications, they’re creating compliance exposure if those outputs don’t meet the Standard 3/4 framework.

Using Unqualified Reviewers

This is more common than it should be. Appraisal reviews must be conducted by individuals who hold the appropriate appraiser credential for the type of property being reviewed. Using unlicensed staff, even experienced mortgage operations professionals, to conduct reviews on loan files is a USPAP violation, full stop.

The credential requirement is also property-type specific. A certified residential appraiser can review a single-family residential appraisal. They cannot review a commercial income property under the same credential.

Inadequate Scope of Work Definition

Every review assignment must define the scope of work for what the reviewer examined, what they didn’t, and why. Vague or absent scope of language is one of the most common deficiencies cited in regulatory reviews and GSE audits.

“Reviewed for USPAP compliance and lender guidelines” is not sufficient for scope language. A compliant scope of a statement specifies the type of review (desk, field, or narrative); the standards being applied; the intended use and users of the review; and any limiting conditions.

Failing to Distinguish Review Opinions from Value Opinions

If a reviewer develops their own opinion as part of the review, that opinion must be developed and reported as a separate appraisal by experienced appraisers.

The rule exists for a reason: a reviewer’s value of opinion carries significant weight in loan decisions. Embedding it in a review report without the full appraisal development framework obscures its basis and creates ambiguity about what was done.

The Fair Lending Dimension

Appraisal review compliance has taken on new urgency in the context of fair lending regulation. The CFPB, HUD, and state regulators have all signaled heightened scrutiny around appraisal bias, and appraisal review is one of the primary mechanisms for detecting and documenting bias-related issues.

An AMC or lender whose review process is robust enough to flag methodological inconsistencies, questionable comparable selection, or neighborhood-based adjustments has a meaningful compliance advantage. One whose review process is a cursory checklist does not.

ECOA and FHA fair lending frameworks increasingly expect institutions to demonstrate active, documented monitoring of appraisal quality, not just a general policy commitment to fair valuation. Your review records are evidence.

Building a Compliant Appraisal Review Program

A well-structured review program has four essential components:

Credentialed Reviewers: Every review is conducted by an appropriately licensed or certified appraiser. Credential verification and maintenance are documented.

Defined Scope Standards: Your review workflow includes standardized scope language that satisfies Standard 3 requirements adjusted for review type (desk vs. field vs. narrative) and property category.

Independent Review Opinions: Reviewers are empowered and expected to form independent professional opinions, not simply validating the original appraiser’s conclusions. Review reports document the basis for those opinions.

Escalation Protocols: Your program defines clear criteria for escalating a desk review to a field review, flagging a report for lender notification, or referring a compliance concern to regulatory authorities.

Without all four components, your review program has gaps, and those gaps will show up in audits.

Why Appraisal Review Is a Business Asset, Not Just a Compliance Cost

The compliance framing is necessary, but it undersells the value of a strong appraisal review function. AMCs that invest in rigorous, well-documented review processes build something the market values: a reputation for quality.

Lender clients don’t just want panels of appraisers. They want partners who can catch problems before they create liability. The ability to demonstrate a documented, compliant review process is a differentiator in AMC business development conversations and a retention factor with existing clients.

For individual appraisers, understanding what reviewers look for is equally valuable. Reports that hold up under rigorous review because the methodology is transparent, the comps are defensible, and the adjustments are supported are reports that build professional reputations over time.

The full picture of what appraisal review involves, including types, components, and best practices, is covered in depth at Go Source Valuation’s appraisal review resource.

Frequently Asked Questions

Q: What is the difference between Standard 3 and Standard 4 in USPAP? Standard 3 governs the development of an appraisal review of what the reviewer must examine, consider, and determine. Standard 4 governs the reporting of how the reviewer must communicate their scope, opinions, and conclusions in writing. Both standards must be satisfied for a review to be USPAP-compliant.

Q: Does every AMC review need to be conducted by a licensed appraiser? Yes. Under USPAP, appraisal reviews are classified as appraisal practice and must be conducted by individuals who hold the appropriate appraiser credential. The specific credential required depends on the property type being reviewed. Residential reviews require a certified general credential at a minimum of a licensed residential credential; commercial reviews require a certified general credential.

Q: Can a lender underwriter perform a USPAP-compliant appraisal review? Not unless the underwriter also holds the appropriate appraiser credential. Mortgage underwriters can and do conduct their own internal evaluations of appraisal reports as part of the loan decision process, but those evaluations are not appraisal reviews under USPAP unless they’re performed by credentialed reviewers applying Standards 3 and 4.

Q: What’s the risk of non-compliant appraisal reviews? Regulatory exposure is real estate appraisal for boards, the GSEs, and federal regulators, all of whom have the authority to examine AMC and lender review practices. Beyond regulatory risk, non-compliant review processes create transactional liability: if a flawed appraisal slips through a non-compliant review process and causes a financial loss, the institution’s liability posture is significantly weaker than if a robust, compliant process had been in place.

Q: How does fair lending compliance connect to appraisal review? Federal fair lending frameworks, particularly ECOA and FHA requirements, increasingly expect lenders and AMCs to demonstrate active monitoring of appraisal quality, including the detection of potential bias indicators. A documented, compliant appraisal review program provides the evidentiary record that regulators expect to see. An absent or superficial review process creates both regulatory exposure and reputational risk.

Q: How should AMCs document their appraisal review process for GSE audits? GSE audit documentation should include review scope definitions, reviewer credential records, written review reports for each reviewed appraisal, escalation logs for reports that triggered elevated review, and any lender notifications resulting from review findings. The documentation should demonstrate a consistent, repeatable process, not ad-hoc reviews triggered only by obvious problems.

Q: What triggers a compliance review versus a standard desk review? A compliance review is typically triggered by specific regulatory risk indicators: appraisals with non-standard scope limitations, reports with unusual or unexplained adjustments, high-LTV transactions, properties in protected-class neighborhoods, or any appraisal where a fair lending concern has been flagged. Lender guidelines often specify the conditions that escalate a routine desk review to a compliance-specific review track.